We continue our series of materials on OEM traffic across regions worldwide. In this article, we turn our focus to...

02 June, 2026

Today, OEM traffic remains one of the key channels for growth, scaling, and maintaining positions in the mobile app market, especially amid increasing competition for user attention. We conducted an analysis of the largest smartphone vendors by region and examined how the structure of OEM ecosystems varies depending on geography, manufacturer market share, and device penetration levels.

OEM traffic has become an important channel for maintaining market share in the mobile industry. Its structure is directly tied to the presence of smartphone vendors in a specific market. At the same time, market sizes and smartphone manufacturers’ shares vary significantly across regions. Analyzing this data helps companies shape commercial strategies, expand their customer base. Moreover, our analysis can improve business performance.

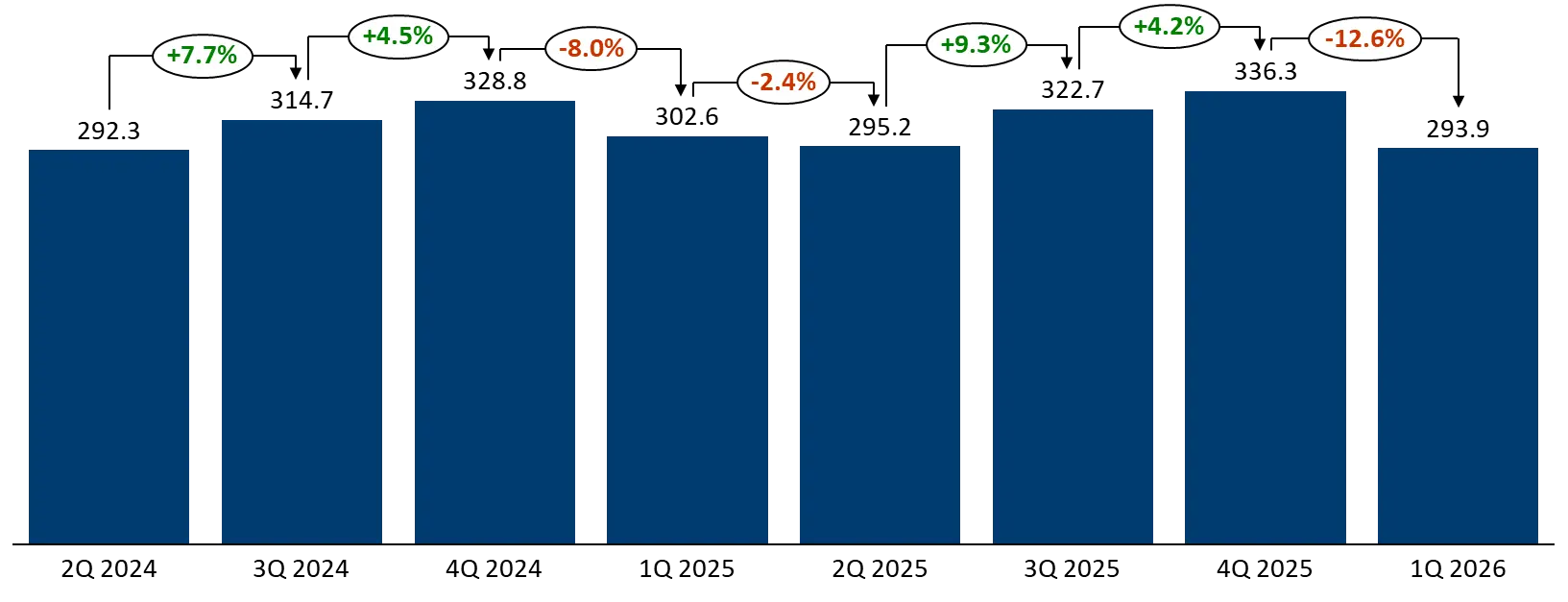

According to IDC, the global smartphone market reached 1.26 billion shipped devices in 2025, showing 1.9% growth compared to the previous year. Growth was recorded across all regions except Asia. In China, sales slowed due to market saturation and increasing competition. Nevertheless, Asia remains the world’s largest smartphone market, with China and India playing a key role. In 2025, these two countries together accounted for 437 million shipped device. It’s 35% of the global volume.

Despite annual growth, global smartphone shipments declined by 2.9% year-over-year in Q1 2026 and by 12.6% compared to the previous quarter. The reason is limited access to memory components, which is driving prices higher. IDC analysts predict that this trend will continue. Although it is likely to affect developing markets more significantly. Developed regions such as North America, which are focused on the premium segment, are expected to be less sensitive to price increases.

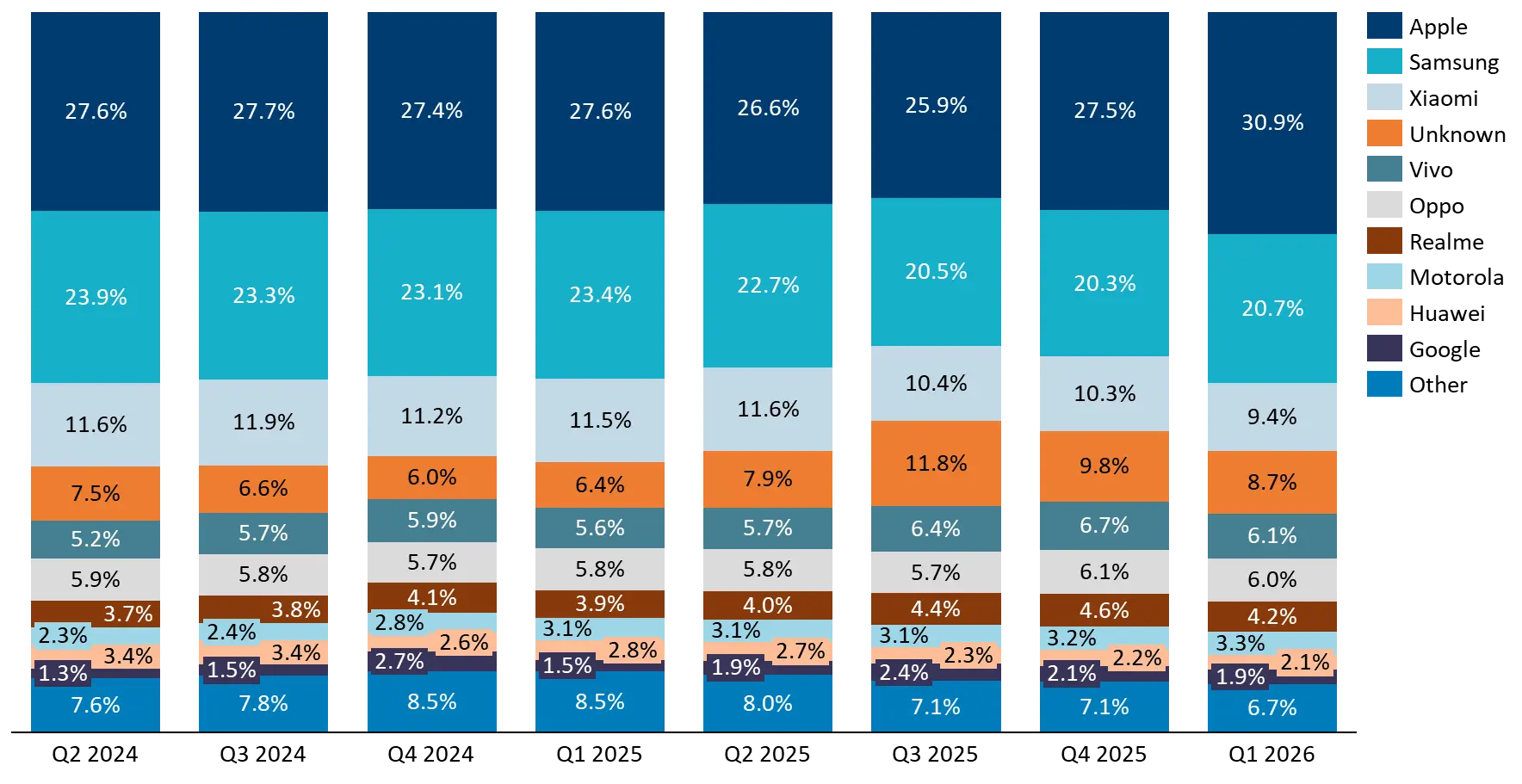

Apple became the global smartphone market leader in Q1 2026. This is driven by the brand’s premium positioning and high level of consumer trust. Apple’s market share increased both in Q4 2025 and Q1 2026 compared to previous periods. Thanks to the successful launch of the iPhone 17, the company captured an additional 3.3% share of the global market in Q1 2026 compared to Q1 2025. It is worth noting that Apple does not use traditional OEM traffic for app promotion.

Samsung ranks second globally with a 21% market share by the end of Q1 2026. The brand leads in South America and Africa, while in Europe and North America, it is second only to Apple. However, Samsung’s global market share slightly declined during Q2 and Q3 2025 due to growing pressure from Chinese brands and Apple’s strengthening position. At the same time, this decline did not affect South America and Africa. From an OEM advertising perspective, Samsung’s key channel is the Galaxy Store app marketplace. There the brand places its main integrations.

Samsung’s Share of Internet Traffic

by Region, Q2 2024–Q1 2026.

Source: Statcounter GlobalStats.

Xiaomi remains among the top 5 smartphone vendors. However, its global market share declined in the second half of 2025 and in Q1 2026. The main reasons were inventory optimization and reduced shipments of older device models. Shipment declines were recorded across all regions except South America.

In the OEM segment, Xiaomi uses the MI Ads platform. Its platform is integrated into multiple system apps and the proprietary GetApps store. Advertising appears in the form of native ads, banners, and full-screen formats.

The “Unknown” segment includes unidentified smartphones whose models cannot be determined. Such devices are commonly found in China, African countries, and Southeast Asia. The sharp increase in this segment’s share in Q3 2025 was driven by growing demand for low-cost devices amid rising smartphone component prices.

Xiaomi’s share of internet traffic

by region, Q2 2024–Q1 2026.

Source: Statcounter GlobalStats.

Vivo and Oppo generally demonstrate stable market performance while maintaining leading positions. Vivo’s market share increased by 0.5% in Q1 2026 compared to the same period last year. Oppo’s share grew by 0.3%. Vivo’s shipment growth was driven by successful integration with Realme and strong performance in China. Oppo continues to grow thanks to its success in China and its strong position in India.

Vivo delivers advertising through its official Vivo Ads network. It’s integrated into the brand’s device interface and pre-installed system applications, including the Vivo Appstore. Ad formats include banners, native ads, full-screen ads, and pop-ups. Advertising on Oppo smartphones is integrated into system applications and the device interface through notifications and recommendations.

The top 10 smartphone manufacturers by user activity also include Realme, Motorola, Huawei, and Google. Realme demonstrated growth in its global market share during the second half of 2025. In Q1 2026, the highest activity for these devices was recorded in Asia, with a 6.9% share.

Motorola has been steadily increasing its global market share in recent quarters. In South America, the brand ranks among the top 5 vendors with a 16.5% share. Globally, demand for Huawei continues to decline, including in its strongest regions such as Africa and Asia, where the brand has traditionally remained popular.

Oppo’s share of internet traffic

by region, Q2 2024–Q1 2026.

Source: Statcounter GlobalStats.

Google’s market share has remained around 2% over the past two years. However, in Q3 and Q4 2025, it increased to 2.4% and 2.7% respectively, driven by the launch of the Pixel 9 and Pixel 10 models. The Pixel 9, in particular, proved highly successful. North America remains the brand’s largest market, where Google’s share reaches 4%.

Other brands include manufacturers such as Infinix, OnePlus, Tecno, Honor, Itel, Sony, Nokia, LG, Lenovo, and others. Collectively, these brands account for a significant portion of the market.

An analysis of smartphone user internet activity over the past two years (Q2 2024–Q1 2026) shows continued market fragmentation, where the leadership of Apple and Samsung coexists with strong competitive pressure from Chinese vendors across multiple regions.

For the advertising market, the key takeaway is the growing importance of OEM channels: built-in advertising networks are becoming an essential monetization tool for top-10 smartphone vendors. At the same time, emerging markets such as Asia, Africa, and South America remain the most vulnerable to rising component prices, which could reshape market share dynamics in the medium term.

Therefore, a successful commercial strategy should take into account not only shipment volumes, but also the regional structure of OEM traffic and the specifics of each vendor’s advertising integrations.

We continue our series of materials on OEM traffic across regions worldwide. In this article, we turn our focus to...

Our international mobile app marketing company has been recognized by MobileAppDaily in four categories. This industry recognition increases our market...